Book on Phenolic Resins Manufacturing Industry

Book on Phenolic Resins Manufacturing Industry. Phenolic Resins Technology Handbook. Production of Phenol-Formaldehyde Resins

Global Phenolic Resin Market is expected to reach an estimated $15.0 Billion by 2022

Phenolic resins or phenol-formaldehyde resins are the synthetic polymers obtained by the polymerization of phenol and formaldehyde. Phenolic resins possess good physical and chemical properties such as high mechanical strength, low toxicity, good heat resistance, low smoke formation and high thermal stability. Due to such high properties, phenolic resins find their applications in myriad industrial products. From molded products such as billiard balls to coatings and adhesives, phenolic resins are used for different applications across various industries such as automotive, electrical & electronics, construction etc. Besides, by mixing phenolic resins with other polymer, they can also be used in applications like corrosion coating, adhesive, etc.

Phenolic resins are employed in a variety of applications such as wood-adhesives, laminates, molding compounds, rubber, and insulation among others. Owing to the favorable physical and chemical properties, phenolic resins have found application in niche segments such as mass-transit, and off-shore oil drilling, which requires materials with high heat resistance.

Applications:

Phenolic resins are used in coatings, composites, adhesives, and in molded parts. The phenolic materials are available in a variety of configurations, for example, with fiberglass and carbon fiber reinforcement or with various fillers and additive combinations, tailored to the requirements of specific industries and applications.

Besides being used in coatings for interiors of food and beverage cans, phenolic resins are an excellent choice for manufacturing protective coatings and for enhancing the performance of epoxy, acrylic, polyester and alkyd based adhesive or coating products. They are, for example, used for tank, drum, and pipe linings; marine and industrial applications; and electrical devices such as wires, motor and wound coils.

Read our Book Here: Epoxy Resins Technology Handbook (Synthesis, Epoxy Resin Adhesives, Epoxy Coatings) with Manufacturing Process and Machinery Equipment Details (3rd Edition)

Due to their low flammability, extremely low generation of toxic gases, and slow heat release, they are often part of solutions for the aerospace and transportation industry. For example, higher glass or carbon fiber content grades are suitable for interior structures of aircrafts. They are also used in products that are exposed to high-temperature and high-pressure environments in industrial and oil and gas applications.

Global Phenolic Resins Market

Construction, automotive, furniture and electrical & electronics industry are the major end-use sectors for phenolic resins. The holistic growth in these industries is expected to drive the demand for phenolic resins in the global market. Phenolic resins find their huge application in different wood products, which is majorly driven by the construction industry growth. The growing construction industry output is further expected to have a positive impact on the global phenolic resins market through 2026. Moreover, increase in demand for various molded products in automotive and aerospace industry is also expected to contribute to the global phenolic resins demand through the forecast period.

Phenolic Resin was the first synthetic polymer to be commercialized and is still a very significant industrial polymer. The demand for Phenolic Resin Market is also driven by the growth in the downstream sector of phenol, which is a raw material for phenolic resins.

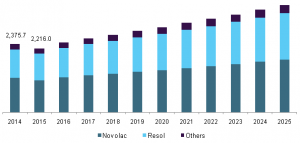

The global phenolic resins market is projected to reach USD 16.0 billion by 2025. High demand for friction materials & rubber in the transportation sector has generated considerable interest in lightweight & durable phenolic compounds, fostering industry growth.

U.S. Phenolic Resins Market Revenue by Product, 2014 – 2025 (USD Million)

The major drivers for growth in this market are increasing use of materials with fire retardant, heat resistant, and anti-corrosive properties in end use applications. Emerging trends, which have a direct impact on the dynamics of the phenolic resin industry, include the development of bio based phenolic resin, and increased penetration of phenolic resin in applications where fire, smoke, and toxicity properties are required.

Wood-adhesive was the largest application segment for phenolic resins and is expected continue in that position in the foreseeable future. The remarkable growth in the building and construction industry in the Asia Pacific and improving scenario in North America has propelled the demand for wood adhesive. Laminates, however, is expected to be the fastest growing application for phenolic resins, owing to the demand for decorative laminates and industrial laminates world-wide. Molding compounds is another application which is expected to register high growth with the increase in application scope. Use of phenolic molding compounds in automotive, marine and off-shore applications has contributed to the growth in this segment. The incremental usage of phenolic molding compounds in automotive in order to reduce fuel consumption and vehicle mass is a driver for phenolic molding compounds.

Global Phenolic Resin Market, By Region, By Value, 2013-2023F

Asia Pacific regions is dominating the phenolic resins market and is anticipated to continue its dominance over the forecast period. The automotive and construction industry are collectively driving the growth of the Asia Pacific phenolic resin market. China and India are the key countries for both automotive and construction industry owing to favorable governmental policies. India is expected to lead this market on account of growing foreign investment in the commercial as well as residential construction projects. Electronics industry in this region is set to develop demand owing to their anti-corrosive and heat resistant properties.

The phenolic resins industry is highly fragmented and dominated by regional players. Some of the major global players include BASF SE, Mitsui Chemicals Inc., Sumitomo Bakelite Co., Ltd., and Georgia Pacific Chemicals LLC among many others. There are several medium sized players in the regional markets.

Phenolic resins are produced from phenol and form an important part of the Indian petrochemical industry. More than 50% of the phenol that is produced is used to manufacture phenolic resins. The industry of phenolic resins is highly organized for it have only a few companies.

Phenolic resin is used in the materials where friction occurs such as brake linings, heavy duty linings, clutch facing, disc pads, railway brake blocks, and gaskets.

The major Indian companies producing phenolic resins are:

- Forace Polymers Pvt. Ltd.

- Asian Lignin Manufacturing Pvt. Ltd.

- Bharat Resins Pvt. Ltd.

- Industrial Resins and Chemicals

- New tech PolymersIndia Pvt. Ltd.

Phenolic Resins Technology Handbook (2nd Revised Edition)

About the Book:

Author: NPCS Board of Consultants & Engineers

ISBN: 9789381039977

Book Code: NI197

Pages: 624

Indian Price: 1,895/-

US$: 150-

Publisher: Niir Project Consultancy Services

Phenolic resins, also known as phenol–formaldehyde resins, are synthetic polymers that are produced from the reaction of phenol or substituted phenol with formaldehyde at high temperatures. These are widely used in wood adhesives, molding compounds, and laminates. The resins are flame-retardant, demonstrate high heat resistance, high tensile strength, and low toxicity, and generate low smoke. In the report, the phenolic resins market is segmented on the basis of product type, application, and region.

Phenolic Resin Market size estimated to reach at USD 19.13 billion in 2026. Alongside, the market is anticipated to grow at a CAGR of 5.4% during the forecast period. The global phenolic resins market has experienced a notable growth and it has been projected that the global market will see stable growth during the forecast period. The high mechanical strengths, low toxicity, heat resistance, low smoke and other several properties has made the phenolic resins to make their use in the applications such as in laminations, wood adhesives, molding compound, construction, automobile and others. Growing demand of these applications has increased the production of phenolic resins to meet the current market demand. Also, phenolic resins is used in flame retardant which is very crucial for automobiles and aircrafts.

This book basically deals with general reaction of phenols with aldehydes, the resoles, curing stages of resoles, kinetics of a stage reaction, chemistry of curing reactions, kinetics of the curing reaction, the novolacs, decomposition products of resites, acid cured resites, composition of technical resites, mechanisms of rubber vulcanization with phenolic resins, thermosetting alloy adhesives, vinyl phenolic structural adhesives, nitrile phenolic structural adhesives, phenolic resins in contact adhesives, chloroprene phenolic contact adhesives, nitrile phenolic contact adhesives, phenolic resins in pressure sensitive adhesives, rubber reinforcing resins, resorcinol formaldehyde latex systems, phenolic resin chemistry, bio-based phenolic resins, flexibilization of phenolic resins, floral foam (Phenolic Foam) with resin manufacturing, lignin-based phenol formaldehyde (LPF) resins, phenol formaldehyde resin, alkaline phenol formaldehyde resin, furfuryl alcohol phenol urea formaldehyde resin, phenol formaldehyde resin (Shell Sand Resin), phenol formaldehyde resin (Cold Box Resin), effluent treatment plant, standards and legislation, marketing of thermoset resins, process flow sheet, sample plant layout and photographs of machinery with supplier’s contact details.

A total guide of phenolic resins and entrepreneurial success in one of today’s most lucrative resin industry. This book is one-stop guide to one of the fastest growing sectors, where opportunities abound for manufacturers, retailers, and entrepreneurs. This is the only complete handbook on Phenolic resins.

See more