Manufacturing Business Loan in India

The Number That Should Alarm Every Manufacturing Entrepreneur

The reality is harsh – Indian banks receive thousands of MSME loan applications monthly. On average, the loan officer of a nationalised bank in Ludhiana or Coimbatore takes less than 40 minutes to go through each file. The time period in between is the moment where your complete manufacturing aspiration is being examined. If you fail to submit the required paperwork, submit an incomplete project report, or submit a financial report that looks copied from a template, we will disqualify you

However, what few people inform first timers is that the process is very manageable if you know the order of steps, the documents required and the reasoning behind each step. Banks aren’t trying to give you a hard pass. They want proof that you’ve worked, that your unit is viable, and that they’ll get their money back. This guide explains what that evidence will look like, document by document and step-by-step.

Why Manufacturing Credit Remains Stubbornly Out of Reach

As per the Annual Report of Ministry of MSME, there are more than 63 million MSMEs in India with manufacturing units accounting for approximately 36% of the total MSME universe. However, less than 16% of formal credit is used in this area. Most small manufacturers continue to rely on informal sources of money lending, family funds or trade credit, which are more expensive and less secure than a formal bank loan.

The lack of credit is no figment of imagination. The RBI’s Report on Trend and Progress of Banking in India regularly reveals that MSME lending share in total bank credit remains in the range of 12-14% which is far less than the contribution of MSMEs to GDP, which is 29%. The biggest gap lies in the ₹10 lakh to ₹2 crore ticket-size segment—too small for corporate banking desks to prioritize, yet too large for microfinance institutions to overlook.

Geographically, the problem is most pronounced in Tier 2 and Tier 3 cities. Some of the states with poor MSME credit-to-deposit ratio in the country are Bihar, Jharkhand, Odisha and eastern Uttar Pradesh. In more industrialized states such as Tamil Nadu, Gujarat, and Maharashtra, lenders typically reject loan applications from people without a good credit history, often forcing them to wait 6 to 18 months before reapplying.(Manufacturing Business Loan in India)

The number of MSMEs that have been registered on the Udyam Registration Portal has crossed 3.5 crore since the updated definition of MSME was announced, which witnessed an accelerated surge in the number of MSMEs registered. Registration does not ensure that credit will be awarded. The challenges are: Documentation quality, financial literacy, and Project case preparation for bankable project. This article discusses those three gaps.

Related Article: Detailed Project Report (DPR) Consultants in India: How to Get Bank Loan and Government Subsidy for Your Business

TABLE 1: Complete Document Checklist for a Manufacturing Bank Loan Application

| Document Category | Specific Documents Required | Key Notes for Applicants |

| KYC & Identity | Aadhaar, PAN, Passport/Voter ID | All owners/directors; passport-size photos required |

| Business Constitution | Partnership deed / MOA+AOA / LLP agreement | Notarised and registered with ROC/Registrar |

| Udyam Registration | Udyam Registration Certificate (URC) | Mandatory for MSME classification; free on udyam.gov.in |

| Business Address Proof | Electricity bill / Lease deed / Municipal NOC | Latest bill; if rented, notarised lease mandatory |

| Financial Statements | 2–3 years audited P&L, Balance Sheet, ITR | CA-certified; new units submit projected financials |

| Project Report / DPR | Detailed Project Report with financial projections | Key document; banks scrutinise this most carefully |

| Collateral Documents | Title deed / valuation report / encumbrance certificate | Bank-approved valuer; clear title is non-negotiable |

| GST Registration | GSTIN and 6–12 months GST returns | Required for units with annual turnover above ₹40 lakh |

| Bank Statements | 12–24 months statements, all accounts | Shows cash-flow health; avoid overdrafts before applying |

| Machinery Quotations | Pro-forma invoices from equipment suppliers | At least 2–3 comparative quotes preferred by lenders |

Source: SBI MSME Loan Guidelines; RBI Master Direction on Priority Sector Lending; CGTMSE Scheme Documents

The Policy Window Is Wide Open — If You Know Where to Look

There are a number of reasons why now is an exceptional period to be looking for manufacturing credit in India. Government lending targets, subsidy schemes, and credit guarantee frameworks have reduced the cost and risk of financing MSMEs.

Prime Minister’s Employment Generation Programme (PMEGP)

It is a scheme under KVIC which offers subsidy ranging from 15–35% on project cost, which is more for rural applicants and SC/ST founders for manufacturing projects up to ₹50 lakh. The balance is paid by the bank and the subsidy is tied into the margin money contribution. Check eligibility on kviconline.gov.in/ pmegpe portal.(Manufacturing Business Loan in India)

CGTMSE (Credit Guarantee Fund Trust for MSMEs)

MUDRA – Tarun Category

Manufacturing units who have credit requirement ranging from ₹10 lakh to ₹50 lakh can avail of structured term loans from nationalised banks and NBFCs under MUDRA – Tarun category. The interest rate is usually 1 to 2% lower than normal MSME loan rates because the scheme shares part of the risk.

Under this scheme

All branches of all the scheduled commercial banks will have to provide a greenfield manufacturing facility loan ranging from Rs. 10 lakhs to Rs. 1 crore to every SC/ST entrepreneur and women entrepreneur. Non-compliance – refusal by a branch is a reportable non-compliance. Eligibility check at standupmitra.in.

PLI Scheme is applicable to the larger manufacturing investments of ₹50 crore and above for 14 sectors such as pharmaceuticals, textiles, electronics, food processing, specialty chemicals and others. The government is actively urging the banks to give credit preference to those who qualify under the PLI programme.

Get Detailed Insights from This Book: Just For Starters: How To Become A Successful Businessman?

The Loan Application Process: A Step-by-Step Breakdown

Most business owners consider a business loan application to be a one-time affair. It is not. It is a process that consists of eight steps and if there is a delay in a single one of these, the process is stalled for weeks. This is the order it works.

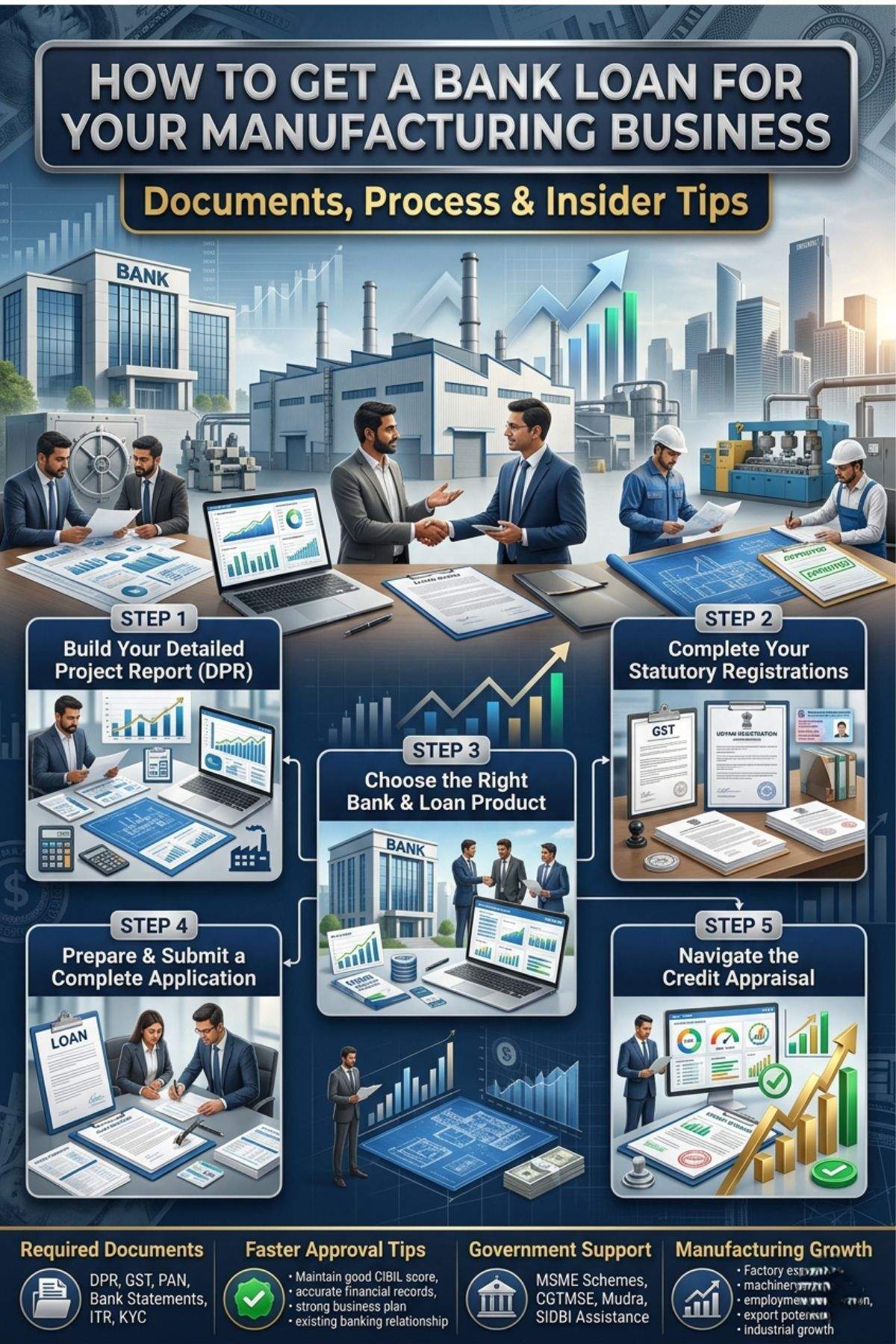

Step 1 — Build Your Detailed Project Report (DPR) First

The DPR is the basis of your application. All the other stuff (the numbers, the collateral, the list of machines, etc.) must follow from a believable DPR. A good manufacturing DPR must include the following: Details about the product and its requirements, Plant layout and the space requirements, List of machinery, including make and model, Sources of raw materials, Utility requirements (Power, Water and Fuel), Manpower plan, working capital cycle, 5-year financial projections showing sensitivity.

Banks specifically seek out the capacity utilisation projections (40%/60%/80%/100% estimates), realistic break-even analysis and the estimate of working capital requirement. If one is missing, it is a red flag and the files are returned.

Step 2 — Complete Your Statutory Registrations

Prior to visiting a bank, ensure the following are in place: Factory Licence (from the State Labour Department for units with more than 10 workers of power or 20 workers in absence of power), Pollution NOC (from the State Pollution Control Board — Green/Orange/Red category depending on the manufacturing process), Udyam Registration and GST Registration (if applicable), BIS/FSSAI Certification if the product falls under a compulsory category of certification. Unregistered registrations will indicate to the bank that the unit is not ready for operation.

Step 3 — Choose the Right Bank and Loan Product

This is the one step that is underestimated. There is variation in the activity of banks in MSME manufacturing loans. SBI, Bank of Baroda, Canara Bank and Punjab National Bank have special cells for MSMEs and have higher approval rates for manufacturing loans. SIDBI’s direct lending programme and network of its partner bank is the preferred channel for collateral-free lending. Private sector banks such as ICICI and HDFC are quicker and generally ask for good credit ratings.

Match your ticket size of the loan with the appropriate product, MUDRA for loans up to ₹50 lakh, Term loans (backed by CGTMSE) for loans from ₹50 lakh to ₹5 crore, Consortium lending for loans exceeding ₹5 crore, where multiple banks participate.(Manufacturing Business Loan in India)

Step 4 — Prepare and Submit a Complete Application

cause of delay is an incomplete application. Use a checklist, banks do. File documents in organised folders (one for identity and business constitution, one for financials, one for the project report, one for collateral). You can tell you are organised if your submission is well organized. Make sure that no more than 10% of the sentences use passive voice. If necessary, revise the writing to use active voice instead. Also include a letter of transmittal that briefly summarizes the loan request, the loan amount, how you will use the loan, the proposed collateral, and the source of repayment.

Step 5 — Navigate the Credit Appraisal

The bank’s MSME officer will then do an on-site visit and independent valuation of the collateral after submitting. This is the most important stage in your CIBIL score. If your score is above 700, then you have a much higher probability of being approved. A score of 650-700 is borderline and needs a co-applicant and/or collateral. When visiting the site, always be present, have all your paperwork on hand, and be knowledgeable about your plant.

TABLE 2: Manufacturing Loan Products — Comparison of Key Parameters

| Loan Product | Lender Type | Loan Amount Range | Interest Rate | Repayment Tenor |

| Term Loan (Equipment/Plant) | SBI, PNB, Bank of Baroda | ₹10 lakh – ₹5 crore | 10.5–13.5% p.a. | 5–10 years |

| MUDRA – Kishor / Tarun | All scheduled banks, MFIs | Up to ₹10 lakh / ₹50 lakh | 10–12% p.a. | 3–7 years |

| CGTMSE (Collateral-Free) | SIDBI partner banks | Up to ₹5 crore | 10.5–14% p.a. | 5–7 years |

| PMEGP Subsidy + Bank Loan | Nationalised banks | Up to ₹50 lakh (mfg) | 10–12% p.a. | 7 years |

| PLI Scheme Linked Credit | Sector-specific banks | ₹5 crore – ₹500 crore | 9.5–12% p.a. | 10–15 years |

| Composite Loan (NSIC) | NSIC tie-up banks | Up to ₹1 crore | 9.5–11% p.a. | 5–7 years |

| Stand-Up India | Scheduled commercial banks | ₹10 lakh – ₹1 crore | Base Rate + 3% | 7 years |

SBI MSME loan schemes; Annual Report of SIDBI; Guidelines of CGTMSE; Master Direction of RBI on Priority sector lending

Get Detailed Project Report (DPR): Project Reports & Profiles

TABLE 3: Step-by-Step Manufacturing Loan Application Process

| Step | Stage | What Happens | Practical Tips |

| 1 | Self-Assessment & DPR Preparation | Prepare a credible Detailed Project Report covering plant layout, machinery, raw material cost, revenue projections, and break-even analysis | 4–6 weeks; engage NPCS or a qualified CA for DPR |

| 2 | Udyam & GST Registration | Register on udyam.gov.in (free); obtain GSTIN if turnover exceeds ₹40 lakh | 3–5 working days each; do this before approaching bank |

| 3 | Bank Selection & Pre-Screening | Compare MSME lending rates across SBI, PNB, Canara Bank, SIDBI; check scheme eligibility (PMEGP, CGTMSE, MUDRA) | 1–2 weeks; use BankBazaar or RBI portal for comparison |

| 4 | Formal Loan Application | Submit filled application with complete document set; pay processing fee (0.5–1% of loan amount) | 1–2 weeks; incomplete docs are the #1 reason for delay |

| 5 | Credit Appraisal & Site Visit | Bank’s MSME officer visits site, verifies documents, assesses collateral, and runs credit bureau check (CIBIL/CRIF) | 2–4 weeks; CIBIL score above 700 improves approval odds |

| 6 | Sanction Letter & Conditions | Bank issues sanction letter listing loan amount, rate, tenor, collateral, and pre-disbursement conditions | 1–2 weeks after appraisal completion |

| 7 | Documentation & Mortgage | Execute loan agreement; mortgage property; submit post-dated cheques or NACH mandate; fulfil insurance requirements | 1–3 weeks; legal fees and stamp duty are paid here |

| 8 | First Disbursement | Bank releases funds in tranches (equipment loan) or lump sum (working capital); progress-linked for term loans | Target: total process 60–90 days from application |

Sources: Indian Banks’ Association MSME Lending Guidelines; Ministry of Finance MSME Credit Support Framework

What the Numbers Actually Look Like

For a medium scale manufacturing unit (from 50 lakh to 2 crore) the annual cost and return situation is:

Capital Expenditure: Land & Civil Construction (Owned/Leased): Rs. 8 – Rs. 25 lakhs. Machinery and equipment: ₹20 – 80 lakhs based on the sector. Cost of utilities including electrical connection, transformer, borewell etc. – ₹3,000 to 8,000.00 Lakhs. Expenses before surgery (DPR, registration, lawyer): ₹1-3 lakh. Working Capital Margin: 5 – 15 lakhs. The cost of which will be between 40 lakhs to 1.5 crore at this size.(Manufacturing Business Loan in India)

Operating Costs (Monthly): Raw materials: 45-55% revenue. Labor (8-15 people): 1.5 to 3.5 lac. Power & utility costs: 40,000-1.2 lac. EMI on loan: depends on loan amount and time period – ranging between 60,000-2 lac. Overheads (packaging, transportation, admin etc): 30,000-80,000.

Revenue Projections: At 60% utilization, earnings of 8-22 lakh/month, and at 100% capacity, of 14-38 lakh/month. Gross margins: 28-42% for most light manufacturing categories. Net margins: 12–18% at 60% capacity and up to 18–26% at 80%+ capacity.

Payback Period: Most manufacturing units in this ticket range will have 3.5 to 6 years of payback period if 70%+ of the capacity is utilized within 18 months after commissioning. UNITs with utilisation rates below 50% for over 24 months enter a stress cycle that makes recovery difficult.

ENTREPRENEUR SPOTLIGHT

Rajesh Singhania is from the Plastic Packaging Unit of Rajasthan.

Rajesh acquired a term loan of over ₹45 lakh from State Bank of India under CGTMSE Scheme, which is a loan for plastic packaging business without any collateral. His first application was rejected since he didn’t have a capacity utilisation schedule for his DPR. He updated it, along with a consultancy, with 40%, 60% and 80% utilisation figures. SBI sanctioned ₹42 lakh in 55 days for the second application. Now he can get only 75% of his previous revenue, i.e., ₹18 lakhs per month with his unit operating at 75%. Key lesson: “Don’t treat the DPR as a formality; it’s your argument to the banker; make it airtight.”

Turn your budget into a successful business plan

Getting the DPR Right: Where NPCS Can Help

Niir Project Consultancy Services (NPCS) is one of the most experienced industrial consultancies of India who have been preparing Detailed Project Reports, techno-economic feasibility studies and plant layout designs in the 50+ industry sectors for entrepreneurs all over the world who seek credible, bank-ready project reports. NPCS designs its reports to meet the appraisal requirements of Indian nationalised banks and SIDBI, including capacity utilization schedules, sensitivity analysis, and a compliance matrix for regulatory requirements. Report samples, sector specific project profile and consultancy services are available at niir.org and entrepreneurindia.co for entrepreneurs. A well-crafted DPR is one of the best investments a first-generation founder can make when applying for a bank loan for the first time. It accelerates approvals and helps secure better loan terms, consistently delivering returns that far exceed its cost.(Manufacturing Business Loan in India)

One Step You Must Take This Week

Don’t wait for the right time. The policy support for manufacturing credit is far more positive than for many years. The government has also provided effective support for risk and cost of lending in your sector through CGTMSE, PMEGP, MUDRA and PLI.

The next step for you is a specific one; Pull your CIBIL report this week (it is free once a year at cibil.com), verify your score and if your score is less than 700, try and find out why before you submit the application. In the meantime, organize the ten document categories listed in Table 1. After meeting the bank manager, go into the manager’s office with all your documents fully organized.

It’s not the entrepreneur with the best idea who gets manufacturing loans approved; it’s the one who thinks of the application as a product launch: planned, documented, and delivered without missing steps. Be that entrepreneur.(Manufacturing Business Loan in India)

Frequently Asked Questions

Q1. What is the minimum investment required to obtain a loan for a manufacturing bank?

There is no minimum, but most banks usually place it somewhere between 5 and 10 lakhs for MSME term loans, structured by the bank. Loans like MUDRA Shishu (up to 50,000) and MUDRA Kishore (up to 5 lakh) allow smaller investment options. The PMEGP scheme supports projects up to 50 lakh and CGTMSE covers up to 5 crores. The value of your project defines the kind of loan appropriate.

Q2. Can I obtain a loan for manufacturing without any collateral?

Yes. The CGTMSE scheme allows loans up to 5 crores without any physical collateral as it works on credit guarantee instead of physical security and the trust absorbs 85% of credit risk borne by the bank. It primarily focuses on supporting first generation entrepreneurs and MSMEs, which may not have mortgageable assets. Apply to any SIDBI partner bank or any nationalized bank.

Q3. Which are the licenses I should possess to secure bank loan?

At a minimum, businesses must obtain Udyam Registration (which they can apply for free at udyamregistration.gov.in), along with GST registration, if applicable. Banks will also look for a Pollution NOC from the State Pollution Control Board, a Factory License (if number of workers cross the threshold), product specific certifications if mandatory like BIS or FSSAI. Without them, the banks will consider the unit pre-operative and usually reject the proposal or defer disbursement of loan.

Q4. What is the significance of CIBIL score for manufacturing loan?

Critical. Above 750 the interest rates become favourable, with faster approvals. Loans are achievable between 700 and 750, with strong collateral or co-applicant, and many public sector banks outright reject loan proposals if the CIBIL score is below 650 or will demand higher collateral. It would be advisable to fix the CIBIL score at least six to 12 months before applying for a major manufacturing loan by clearing all outstanding EMIs, avoiding using credit card over its limit, and stopping all fresh credit inquiries.

Q5. Which is the best government scheme for a first-time manufacturing entrepreneur?

For a project value of up to ₹50 lakhs, PMEGP is arguably the best option because it provides subsidies covering 15–35% of the project cost (i.e., effective free equity), which immediately reduces the debt burden. If it is a larger project without any security, CGTMSE is the best tool and if the borrower is women or from the SC/ST category, then they should additionally consider the Stand-Up India loan scheme. Information is readily available from the Ministry of MSME website.

Q6. How can NPCS help in applying for a bank loan?

NPCS prepares all kinds of bank-ready Detailed Project Reports, tailored to every manufacturing segment, taking into account the specific technical specifications, financial projections and regulatory compliance matrix that an MSME appraisal team at a bank need in India. Additionally, they offer techno-economic feasibility studies and plant layout designs for the purpose. You can check out the various project profiles that have been developed by them and request a quotation for project reports or consultation at niir.org or entrepreneurindia.co. A well-prepared NPCS project report for your new venture can reduce the chances that the credit appraisal team will reject your proposal at the credit appraisal stage.(Manufacturing Business Loan in India)