Steel Manufacturing Plant Setup in India: PLI Benefits

India’s Steel Sector Signals a $500 Billion Business Window — What It Means for You

The Indian government stealthily remapped one of its most critical industries. The Press Information Bureau (PIB) had put out a detailed backgrounder in May 2026 from the Ministry of Steel that India has now entered the second half of the league table as the second largest producer of steel and second largest consumer in the world, and that the Government is moving fast on policies to maintain this position and reach a target of 500 million tonnes by 2047.

Not a regular change update. The data show a sector going through a structural change, where finished steel demand has increased from 77 MT in 2014-15 to 163.7 MT in 2025-26. Crude steel output has grown at a 9% CAGR since 2021–22, reaching 168.4 MT in FY 2025–26. Steel exports jumped 35.80% in FY 2025–26 while imports crashed by 46.47%. Under the Production Linked Incentive (PLI) scheme, ₹23,022 crore has been mobilised till now, and 13,264 jobs have been created in the field and 2.4 MT of specialty steel produced.

For entrepreneurs, MSMEs, manufacturing and startups and investors, it is the once-in-a-decade inflection point. The government has created a thick, forest of incentives, preferential procurement, quality regulations, and green transition mandates to create investable gaps along the steel value chain. Specialty steel production, scrap recycling, integration of green hydrogen, and AI-driven quality management are among the opportunities, layered, tangible and supported by sovereign policy momentum.

India’s Steel Industry: Sector Overview

The Government of India has identified steel as a ‘Sunrise Sector’ and it is expected that the growth of this sector will exceed the overall economic growth. The Indian steel sector is a large, diverse industry with iron ore mining, pelletisation, sponge iron and pig iron production, electric arc furnace (EAF) steelmaking, blast furnace operations, hot and cold rolling and downstream value-added processing like coating, wiring and alloying.

It covers 12 major steel zones including Kalinganagar, Angul, Rourkela, Jharsuguda, Nagarnar, Bhilai, Raipur, Jamshedpur, Bokaro, Durgapur, Kolkata and Vizag with the fast development of rail, road and port infrastructure under the aegis of PM GatiShakti. There are more than 2100 steel units that are active and geo-tagged on PM GatiShakti platform for logistics planning. 68% of the domestic steel consumption goes into construction and infrastructure, 22% to engineering and packaging and 9% to automobiles.(Steel Manufacturing Plant Setup in India: PLI Benefits)

Download the Full Guide: Steel and Iron Handbook

Market Growth Analysis: Numbers That Define the Opportunity

The growth narrative is clear. India’s share of global crude steel output rose from 5.2% in 2014 to 7.9% in 2024. Crude steel production is expanding at a CAGR of 9%, while finished steel consumption has reached 163.7 MT in FY 2025–26, an increase of 7.6%, compared to the previous year. Outbound finished steel shipments rose 35.80% during the same year, more than half of which was shipped to Vietnam, Belgium and Taiwan.

India is already 66% towards the production target – 300 MTPA crude steel capacity and 255 MTPA production – with per-capita consumption of finished steel to go up from 61 kg to 158 kg by 2030-31 – which means the remaining 34% – an addressable investment universe of tens of thousands of crores of greenfield and brownfield capacity.

The longer arc is even more interesting. The target of 500 MT of steel production capacity by 2047 – Viksit Bharat – translate to an increase of about three times the current capacity over the next 20 years. The structural demand is a guarantee of the viability of new players across the steel value chain.

Key Steel Sector Performance Data (FY 2022–23 to FY 2025–26)

| Metric | FY 2022–23 | FY 2023–24 | FY 2024–25 | FY 2025–26 | Growth (YoY) |

| Crude Steel Production (MT) | 127.2 | 144.3 | 152.2 | 168.4 | +10.7% |

| Finished Steel Production (MT) | 123.2 | 139.2 | 146.7 | 160.9 | +9.7% |

| Finished Steel Consumption (MT) | 119.9 | 136.3 | 152.1 | 163.7 | +7.6% |

| Steel Exports — FY 25–26 Growth | — | — | — | — | +35.80% |

| Steel Imports — FY 25–26 Change | — | — | — | — | –46.47% |

| Hot Metal Production (Apr–Sep) | 43.99 MT | — | — | 47.21 MT | +7.3% |

| Sponge Iron Production (Apr–Sep) | 27.00 MT | — | — | 29.46 MT | +9.1% |

| PLI Investment Realised | — | — | — | ₹23,022 Cr | — |

| Direct Jobs Created (PLI) | — | — | — | 13,264 | — |

| Green Steel Certified Units | — | — | — | 89 units | 12.34 MT |

| Specialty Steel Capacity (PLI) | — | — | — | 24 MT | — |

| Import Substitution Achieved (PLI) | — | — | — | ₹6,000 Cr | — |

Government Policies & Incentives: The Business Case in Policy

PLI Scheme for Specialty Steel (PLI 1.0, 1.1, and 1.2)

The PLI scheme for specialty steel offers 4% to 15% incentives towards incremental sales for five years. The new PLI 1.2 includes 85 applications, falling into four product categories: Strategic grades, commercial grades (Category 1 & 2), and coated & wire products. As per MoUs for PLI 1.2, a commitment of ₹11,887 crore has been made and the capacity is being added of ~8.29 MT. The next two years are perfect for new applicants to establish and qualify for incentive disbursements, which will start in FY 2026–27.

Get Detailed Project Report (DPR): Steel, Iron & Alloy Steel Reference Guide

DMI&SP Policy (Revised May 2025)

The Domestically Manufactured Iron and Steel Products policy stipulates that the government will give preference to Indian steel in government contracts. India’s infrastructure pipeline is estimated to be worth hundreds of lakh crore rupees, meaning that this policy will ensure a guaranteed domestic market for compliant manufacturers, which will be a huge boon for new steel fabricators and processors.(Steel Manufacturing Plant Setup in India: PLI Benefits)

12% Safeguard Duty on Steel Imports (April 2025)

Ensures that the domestic producers of selected non-alloy and alloy steel flat products are not subject to import surges through a 12% safeguard duty. This directly helps Indian steel manufacturers, in particular the mid-scale producers, who were facing subsidised Asian imports.

Mission Coking Coal & Raw Material Security

Mission Coking Coal (2024) aims to produce 140 MT of domestic coking coal by FY 2029-30 and cut down the dependency on imports by 65% by FY 2030-31. It reduces costs for integrated steel companies and provides ancillary coal logistics and beneficiation enterprises.

CCUS Budget Allocation: ₹20,000 Crore

Union Budget 2026-27 provides a total of ₹20000 crore for 5 years for the CCS technologies. It is a clear warning to the tech industry, engineering startups, and industrial service providers developing CCUS solutions for steel plants that this represents a market being backed by the government.(Steel Manufacturing Plant Setup in India: PLI Benefits)

Manufacturing Opportunities: Where Capital Should Flow

The government’s policy framework produces four separate manufacturing opportunity zones:

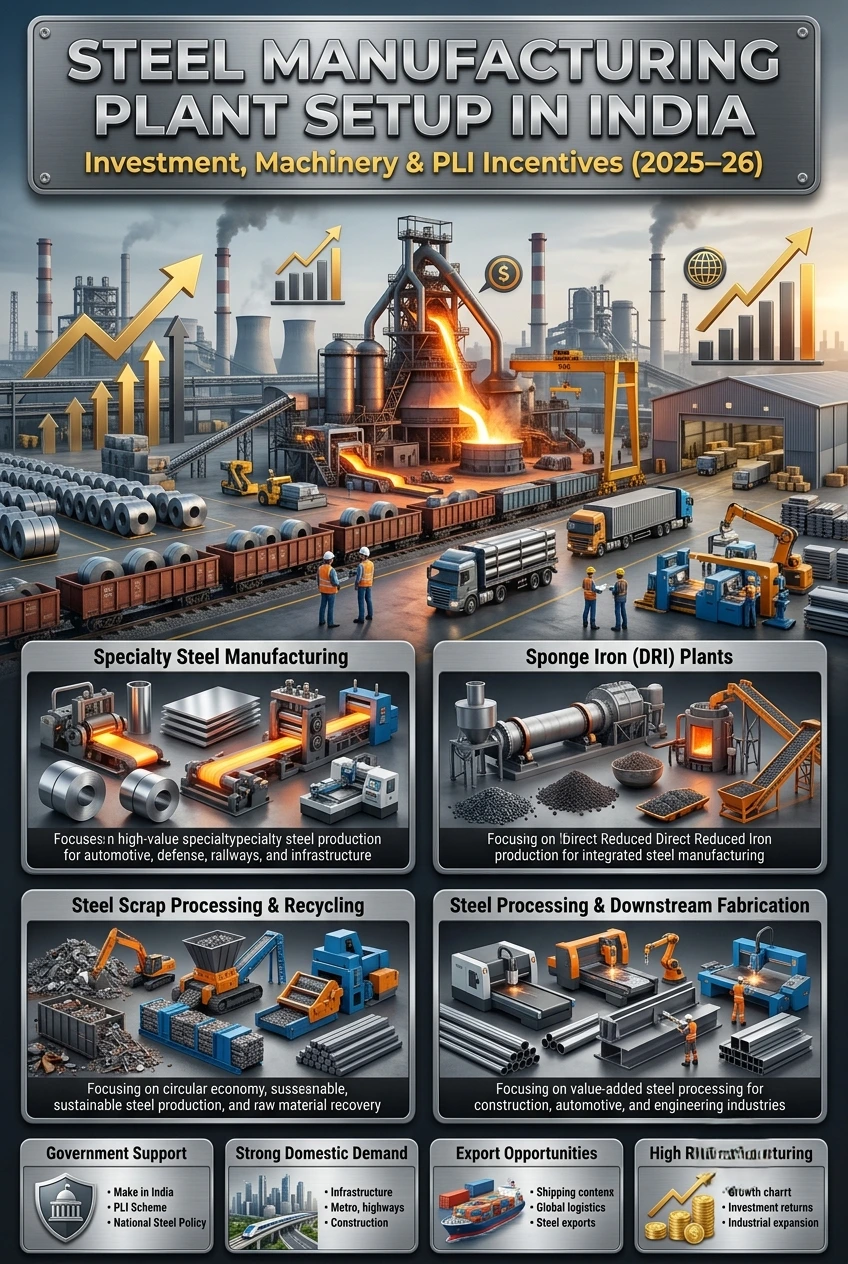

1. Specialty Steel Manufacturing

In terms of products, it is seen that the imports of coated steel, electrical steel, alloy steel and high strength steel for automotive and defence applications are high-margin. The PLI scheme provides direct financial benefit, and import substitution worth a whopping ₹6,000 crore has been proved by early adopters. One of the most government supported manufacturing investments today is a new specialty steel plant of 50,000 – 100,000 tonne/annum capacity suitably located within designated steel zones.

Related Article: Is Steel Manufacturing Still Profitable in India? A DPR Analysis

2. Sponge Iron (DRI) Plants

DRI (DRG) or Sponge Iron is an important raw material for Electric Arc Furnace. Production grew 9.1% in H1 FY 2025–26. The drive for green hydrogen-based DRI – replacing natural gas with hydrogen – opens up an early window of opportunity for startups to establish DRI capacity with readiness for green hydrogen. Pilot projects by the government, for hydrogen injection in DRI, are already being implemented.

3. Steel Scrap Processing & Recycling

Indian consumption of steel scrap is about 30 MT per annum with about 5 MT being imported. Domestic scrap supply is being encouraged through the aforementioned Steel Scrap Recycling Policy (2019) and Vehicle Scrapping Facility rules (2021). The result of scrap-based steelmaking is 58% fewer emissions of greenhouse gases and 40% less water usage. Establishment of Registered Vehicle Scrapping Facility (RVSF) or ferrous scrap processing plant (FSPS), more particularly in the locations close to the automotive hubs and tier-2 cities, is considered as capital efficient and policy supported play.(Steel Manufacturing Plant Setup in India: PLI Benefits)

4. Steel Processing & Downstream Fabrication

The value-addition feeder that transforms hot-rolled coil into construction, packaging and engineering products is structural steel fabrication, precision tubes, wire drawing, galvanising and coating. Margins are product orientated and process oriented here and makes it a perfect segment for MSMEs which have the benefit of being in industrial clusters.

Startup Opportunities: Technology & Services in the Steel Ecosystem

Government’s AI in Steel Pavilion initiative explicitly puts the industry in a place where startup solutions can be sought to address the actual problems in the industry. It’s a structured area for tech startups to enter the market of steel producers and AI, IoT, and analytics solution providers. Specific opportunities include:

- AI-based steel plant defect detection system, thickness measurement system, and surface inspection system.

- Both carbon footprint monitoring and green steel certification SaaS platforms are becoming a necessity. The monitoring and certification of carbon footprint using SaaS and the green steel platform are becoming required.

- Equipment IoT solutions for blast furnace/rolling mill operations – prediction maintenance

- Technology and solutions for the green hydrogen supply chain and logistics.

- Digital procurement platform, price discovery platform for MSMEs for steel

- Compliance with new emission norms monitored & reported using CCUS software

- Steel scrap marketplace and aggregation centres and linking mini steel plants to steel scrap selling points

The Green Steel Taxonomy (2024) marks India’s first Green Steel Taxonomy. It creates opportunities for certification consultants, energy auditors, and sustainability report consultants through 89 certified green steel units. These professionals can offer services such as energy audits and sustainability reporting with relatively low investment requirements.(Steel Manufacturing Plant Setup in India: PLI Benefits)

MSME Opportunities: The ₹10 Lakh to ₹10 Crore Entry Window

The government’s reform package explicitly mentions MSMEs and small steel players as beneficiaries. Here are some tips on how smaller players can play in:

- Steel Fabrication Units: produce steel structural elements, pre-engineered buildings and industrial shelving in infrastructure and construction (which is the largest steel consuming industry accounting for 68% of the demand).

- Wire Drawing and Cold Rolling: Process hot-rolled rod into galvanised and stay wire, binding wire, PC strand and other products with high demands in rural areas and construction sites.

- Steel Service Centres: Cut to length, slitting, blanking and other operations used by the downstream manufacturers who do not spend on integrated steel processing.

- Precision Tube Manufacturing: Supply to automotive, HVAC and plumbing industries — relevant to automotive clusters around Pune, Chennai, Gurugram and Sanand.

- Steel Scrap Dealerships and Collection Centres: Ferrous industrial and post-consumer aggregates for supply to mini steel plants based on EAF.

- BIS Compliance Consulting, Laboratory Testing and Certification: BIS services are growing and growing; with 143 Quality Control Orders covering 723 steel products.

SIDBI and NSIC provide standalone credit facilities/support facilities for MSMEs of the steel sector. The MSME ministry introduces Udyam registration platform, which extends access to Government preference for MSMEs under the DMI&SP policy.

Import–Export Opportunities: The Trade Reversal Story

India’s trade data in steel is marking a significant structural transformation. Steel exports grew 35.80% in FY 2025–26; imports fell 46.47%. Vietnam, Belgium and Taiwan are the three largest markets accounting for more than 50% of finished steel imports. Market access is going to be further increased by pending Free Trade Agreements with the UK and European Union.

Export Opportunity: High value segments are specialty steel, coated products, high strength wire rod, stainless steel and electrical steel. The PLI 1.2 scheme is influencing export volumes to increase by over 3x by 2029–30 from 2023–24. Exporters who are registered under DGFT, having EEPC India membership, are eligible for Market Development Assistance and preferential freight scheme.

So far, the government has achieved ₹6,000 crore of import substitution through PLI and has massive room for further growth. There are still large import shortages for high-grade automotive, electrical, and specialty alloys. Both the safeguard duty protection and the DMI&SP procurement preference will work in favour of manufacturers who can offer these products of domestic origin of a satisfactory quality on a competitive basis.(Steel Manufacturing Plant Setup in India: PLI Benefits)

Input cost advantage for nickel alloy and molybdenum steel manufacturers: The government has removed the Basic Customs Duty on Ferro Nickel and Molybdenum ores, giving manufacturers a direct advantage by reducing their input costs. The importers and distributors of these speciality ores to alloy steel producers have a new commercial opportunity.

Raw Materials: Sourcing Strategy for Steel Businesses

| Raw Material | Primary Source | Policy Benefit | Business Relevance |

| Iron Ore | Odisha, Jharkhand, Chhattisgarh | Domestic availability; state mining leases | Core input for integrated steel plants |

| Coking Coal | Jharkhand, Chhattisgarh | Mission Coking Coal targets 140 MT by FY30 | Critical for blast furnace operations |

| Sponge Iron (DRI) | Domestic production | Growing output; hydrogen-based DRI pilot | Feedstock for EAF mini mills |

| Ferro Nickel | Imported (Duty = 0) | Zero customs duty as of Union Budget 2024-25 | Alloy and stainless steel manufacturing |

| Molybdenum Ore | Imported (Duty = 0) | Zero customs duty as of Union Budget 2024-25 | High-strength and tool steel production |

| Steel Scrap | Domestic + Import (~5 MT) | Scrap Recycling Policy; VScF rules 2021 | EAF steelmaking; green steel transition |

| Pellets | Domestic pellet plants | Ministry push to raise pellet usage | Blast furnace and DRI charge material |

| Lime/Dolomite | Rajasthan, MP, UP | Widely available domestically | Flux and slag-forming agent in steelmaking |

Machinery Overview: What You Need to Set Up

There are significant differences across the steel manufacturing machinery segments. The following is a useful summary of some important business opportunities:

For Sponge Iron (DRI) Plant (50,000 TPA)

- Rotary kiln (50-100 m length) with cooler, ESP (Electrostatic Precipitator)

- Coal feeding and Iron Ore crushing systems

- Warm waste heat recovery boiler

- Material handling conveyors and screening plant

Operational capex: ~ ₹3,000/- per ton (per unit based on 300 ton/day capacity)

For Steel Fabrication & Rolling Unit (MSME Scale)

- Rolling mill (bar/rod/section mill): ₹3-15 crore (as per capacity)

- Melting of scrap in induction furnace (5–20 tonne): ₹1.5–5 crore

- Refining furnace for quality improvement (ladle)

- Continuous casting machine (billet caster)

- Straightening, cutting & bundling machines

For Steel Scrap Processing Plant

- Liquidators and baling machines

- Shredder and magnetic separation systems

- A conveyor system consisting of a series of conveyors that are used to sort and grade scrap.

Estimated capex: ₹50 lakh to ₹3 crore for mid-scale scraps processing plant.

Find high-return business ideas based on your budget & ROI

Manufacturing Process Overview

The steel industry in India has two major routes:

Route 1: Blast Furnace – Basic Oxygen Furnace (BF-BOF)

Iron Ore + coking coal → Hot metal (Blast Furnace) → Liquid steel (BOF) → Continuous casting (CC) → Hot rolling (HR) → Finished products. It is suitable for large integrated plants (1 MT+). Capital intensive (₹5,000-15,000 crore for greenfield) and has the widest product range.

Route 2: Electric Arc Furnace (EAF) / Induction Furnace

Scrap / Sponge Iron → Melting (EAF / IF) → Refining → Continuous Casting / Rolling. Ideal for mini steel plants (50,000–500,000 TPA). These projects require lower capex (₹50 crore to ₹500 crore), have a shorter gestation period, and naturally support the green steel transition by using electricity instead of coking coal.(Steel Manufacturing Plant Setup in India: PLI Benefits)

Green Steel Route (Emerging)

Direct Reduced Iron (DRI) via Electro Arc Furnace (EAF) from Green Hydrogen + Iron Ore. Pilot projects are being implemented by the government. Certifiable against Green Steel Taxonomy and monetisation for carbon. Best for the early movers who have long-term green transition vision.

Investment Opportunities: Entry Points Across Capital Ranges

| Investment Range | Business Type | Expected Returns | Risk Profile |

| ₹25–75 lakh | Steel scrap collection & processing unit | 18–25% ROI | Low–Medium |

| ₹1–5 crore | Steel fabrication / structural unit | 20–28% ROI | Low–Medium |

| ₹5–25 crore | Wire drawing / cold rolling / galvanising plant | 22–30% ROI | Medium |

| ₹25–100 crore | Induction furnace + rolling mill (mini steel plant) | 18–24% ROI | Medium |

| ₹100–500 crore | Specialty steel processing plant (PLI-eligible) | 20–30% ROI + PLI | Medium–High |

| ₹500 crore+ | Sponge iron / integrated DRI + EAF steel plant | 15–22% ROI + PLI | High (long gestation) |

| ₹5–50 lakh (Tech) | Steel-tech SaaS / AI quality / certification startup | High (equity value) | High (market risk) |

FDI into metallurgical industries has totalled USD 18.67 billion between April 2000 and June 2025 under the 100% automatic FDI route. PE and VC funds are also increasingly active in green steel and circular economy sub-sectors.

6 High-Potential Business Ideas from This PIB Announcement

1. Specialty Steel Coating & Galvanising Plant (PLI-Eligible)

There are four categories of PLI 1.2 (Product Line Information) products: coated and wire products, paper products, printing and copying products, and audio-visual products. A galvanising/colour coated steel sheet plant located in a close proximity to a major steel zone would be eligible for PLI of 4%-15%. Investment range: ₹15–80 crore. Target markets: roofing, white goods, automotive OEMs, infrastructure construction.(Steel Manufacturing Plant Setup in India: PLI Benefits)

2. Registered Vehicle Scrapping Facility (RVSF)

Set up a RVSF utilising Vehicle Scrapping policy (2021) and the Steel Scrap Recycling policy (2019). End-of-life vehicles are taken apart, iron-steel parts are shredded and the scrap is sold to EAF steel plants. Incentive for vehicle owners to scrap old vehicles provided by the government is Certificate of Deposit (CoD). Investment: ₹1–5 crore. Revenue: sale of scrap + transaction fees for CoD.

3. Green Hydrogen-Ready DRI Consulting & Engineering Firm

With a growing government drive to inject hydrogen into the DRI process, the steel mills are going to require engineering partners who know the DRI process and also have expertise in the area of hydrogen safety. A small engineering and project management firm specialized in hydrogen-DRI integration could access a large amount of consulting opportunities for a nominal cost of starting up.

4. Steel BIS Compliance & QCO Advisory Services

Manufacturers require assistance dealing with BIS certification documents, testing procedure and documentation for import compliance on 143 QCOs for 723 steel products. A specialised QCO consulting practice provides support to steel importers and domestic producers and end-users requiring compliant procurement. Low capital expenses, high premium for expertise.(Steel Manufacturing Plant Setup in India: PLI Benefits)

5. Steel Price Discovery & MSME Procurement Platform

MSMEs purchasing steel in small quantities end up paying much higher premiums than large buyers. A digital solution that brings together the demand from small manufacturers, gets them bulk rates and makes them just in time delivery can create commission profits and actual savings. Imagine a version of ONDC for steel procurement for industries.

6. Carbon Footprint Monitoring SaaS for Green Steel Certification

To comply with India’s Green Steel Taxonomy, plants must show CO2 emission intensity of less than 2.2 tonnes/tonne of finished steel. Only 89 plants are certified so far. A SaaS solution that helps hundreds of steel units track energy consumption, calculate emissions, and prepare certification reports can support their journey toward green certification and help them access ESG-focused export markets in Europe and the UK.

Risks & Challenges: Entering with Eyes Open

Coking Coal Dependency

Even after the Mission Coking Coal, the Indian demand for coking coal is still 85% met from imports. Price volatility of coal at global level directly affects the integrated steel plant margins. For new entrants, it is possible to minimise this through EAF based routes.

Capital Intensity & Gestation

The industry of steel making requires a lot of capital and long gestation period (2-4 years for large plants). Financial planning and alignment of PLI disbursements is a critical part of debt servicing during the pre-revenue stage.

Environmental Compliance

Air, water and solid waste management are more and more being held under the spotlight in the field of steel. Pollution is controlled to high standards for new plants. In the medium term, the green steel standards will gradually be binding, which will involve capex spending on technology upgrades.(Steel Manufacturing Plant Setup in India: PLI Benefits)

Quality Control Order Compliance

The 143 QCOs covering 723 products indicate that authorities do not allow poor-quality products to enter the country and require domestic manufacturers to follow rigorous quality standards. Failure to comply may lead to product recall and ban on access to the market, particularly for the small producers equipped with old equipment.

Global Trade Dynamics

The Chinese overcapacity is still affecting the world steel prices. India has a safeguard duty of 12%, but FTA negotiations may lead to competition. It is important for export companies to be aware of developments in target markets relating to anti-dumping.

Indian Success Stories: Proof Points for the Opportunity

Tata Steel — Green Steel Leader

Tata Steel’s Jamshedpur plant, one of the oldest integrated steel works in Asia, has proactively invested in green steel technologies such as waste heat recovery, scrap-based steelmaking, and renewable energy integration. Steel Europe has pledged to hydrogen steelmaking, bringing back technology insights for steelmaking in India. The company’s early application of the best available technologies is exactly the government’s mandate to promote BAT.(Steel Manufacturing Plant Setup in India: PLI Benefits)

JSW Steel — PLI Beneficiary & Export Champion

JSW Steel, Mumbai is India’s leading private sector steel producer. The company is the most competitive bidder and the market leader among steel players in PLI Scheme for Specialty steel. The company has invested in high-strength steel for automotive and Cold Rolled Grain Oriented (CRGO) electrical steel that are under the PLI ambit and represent a substantial opportunity for import substitution. With exports in 100 plus countries, the company is commercially proven in its export-led model.

Godawari Power & Ispat — MSME to Mid-Cap Journey

The company which is located in Chhattisgarh, India began as a manufacturer of Sponge Iron and then expanded into a complete steel plant with various stages of capacity enhancement.

Today, the company stands as a publicly listed mid-cap enterprise, showing how a focused sponge iron and steel business in a resource-rich state can achieve systematic growth over two decades.

Shyam Metalics — Scrap to Steel

Shyam Metalics & Energy, now a listed company, built a significant business in ferro alloys, sponge iron, and long products in West Bengal and Odisha. Its journey reflects how vertically integrated steel businesses — starting from raw material processing — can capture margin across the value chain.

How NPCS Can Help You Enter the Steel Business

Technical, financial, and regulatory considerations can all seem like a daunting challenge when you’re an entrepreneur or investor looking to enter the steel industry. That’s where NPCS (Niir Project Consultancy Services) can play a vital role.

With regards to steel sector feasibility reports, detailed project reports (DPRs), plant layout designs, quotation for machinery and plant and market research, NPCS provides a comprehensive solution to all kinds of steel sector unit, be it a sponge iron plant, an induction furnace unit, a specialty steel processing unit or a scrap recycling unit. NPCS has more than 5,000 project reports across various industries, making it a trusted source for promoters aiming for bank-friendly, investor-ready paperwork.(Steel Manufacturing Plant Setup in India: PLI Benefits)

NPCS project reports support you with every financial and technical requirement, from preparing PLI applications to securing financing through SIDBI or nationalised banks. These reports help you prepare loan documents and meet the requirements for bank funding. They present steel sector reports that include raw material sourcing data, machinery specifications, manufacturing process flows, cost of production, break even analysis and financial projections based on the market realities.

Key Government Resources

- PIB Press Release — India’s Steel Sector Advances Towards Self-Reliance: https://www.pib.gov.in/PressReleasePage.aspx?PRID=2258028

- Ministry of Steel — Official Website: https://steel.gov.in

- DPIIT — PLI Scheme Details: https://www.dpiit.gov.in

- Startup India — Steel Tech Ecosystem: https://www.startupindia.gov.in

- Make in India — Steel Sector: https://www.makeinindia.com

- EEPC India — Steel Exports Promotion: https://www.eepcindia.org

Frequently Asked Questions (FAQs)

Q1. Who can apply for the PLI scheme for specialty steel and what is it?

Specialty steel benefits under PLI scheme is financial incentive of 4%-15% on incremental sales for 5 years. With the introduction of PLI 1.2 in November 2025, 85 applications have been accepted in four categories of products (strategic grades, commercial grades (Category 1 & 2), coated & wire products). Eligible applicants are Indian incorporated companies with manufacturing units with minimum investment and production. The government will disperse the first round of funds in FY 2026–27, making it a good time to apply for upcoming rounds of the incentive.

Q2. What is the capital required for establishing the business of steel in India?

There are considerable differences in investment needs among segments. The cost of establishing a steel scrap processing unit is ₹50 lakh-₹3 crore. The cost for an MSME scale fabrication or wire drawing plant is ₹1 – ₹10 crore. The investment required for a mini steel plant with induction furnace and rolling mill is around ₹25–150 crores. A PLI eligible specialty steel processing plant would need an investment of ₹100 crores and more. Product development investments are as low as ₹20-50 lakh for tech startups that are tackling problems faced in the steel industry.

Q3. What is Green Steel and is there a business opportunity in it?

CO2 emission intensity of Green Steel is below the 2.2 tonnes of CO2e per tonne of finished steel as per India’s Green Steel Taxonomy (2024) – the world’s first official taxonomy. Green steel business opportunities include clean steel opportunities in steelmaking (S-steel, hydrogen-based DRI), clean steel services (such as carbon monitoring, carbon certification training and support) and clean steel technology (such as carbon tracking saas solution, carbon capture utilization solution, and carbon tracking logistics for green hydrogen). The government has provided funding of ₹20,000crore for CCUS technologies and is operating 4 pilot hydrogen projects in the steel industry.

Q4. How is the safeguard duty helping domestic steel manufacturers?

The Government of India in April 2025, introduced a 12% safeguard duty on certain non-alloy and alloy steel flat products. This safeguards domestic producers against an influx of imports from low prices, especially from China and Southeast Asian countries, by increasing the “landed” price of imports that compete with domestic products. This, coupled with DMI&SP policy of preference for steel from domestic sources in Government procurement, gives a structurally protected domestic market to steel producers in India. This essentially contributes to the improvement of working capital cycles and the realization of prices for MSMEs and small producers.

Q5. What options does an MSME have to enter the specialty steel segment under PLI scheme?

Yes, although PLI is more of the scheme for larger manufacturers with huge investment plans, MSMEs can take part in the specialty steel value chain supplying as a downstream processor, conversion agent or making components for PLI registered manufacturers. Moreover, SIDBI provides a range of specialised credit schemes and NSIC provides raw material assistance to MSMEs engaged in the steel industry. The entire steel value chain, including service centres, fabrication plants, testing laboratories, as well as logistics companies, is open to MSMEs, and is not PLI qualified.

Q6. What are the important zones of steel in India and why location is important?

The 12 major steel zones are: Kalinganagar, Angul, Rourkela and Jharsuguda (Odisha); Nagarnar (Chhattisgarh); Bhilai and Raipur (Chhattisgarh); Jamshedpur (Jharkhand); Bokaro and Durgapur (West Bengal/Jharkhand); Kolkata (West Bengal); and Vizag (Andhra Pradesh). The significance of location of these zones is that the government has given special preference to the development of rail, road and port under PM GatiShakti specifically to these clusters. Close proximity to raw material supply (iron ore, coal), a trained workforce, logistics connectivity directly influence production cost and delivery time, which is crucial for margin management in commodity-driven market.

Conclusion: The Steel Opportunity Is Not Coming — It Is Already Here

The Indian steel industry is no longer a ‘speculative game’. The government supports this data-driven, policy-backed expansion engine, which is creating opportunities for new manufacturing capacity, technology collaborations, and service providers across its entire value chain.

The PIB announcement in May 2026 is not a press release; it is a strategic investment alert. All the data points suggest a single thing: India’s steel ecosystem needs entrepreneurs, manufacturers, startups and investors to be at the forefront of the opportunity.

The window is open. The 500 MT target for 2047 implies about a threefold increase in steel production in the next 20 years. Whether the entrepreneur is starting a scrap recycling business, a specialty steel business, a green certification SaaS or a business providing BIS compliance consultancy, they are entering a market where sovereign tailwinds have been in motion, the demand is structural and the raw material and logistics ecosystem has improved.(Steel Manufacturing Plant Setup in India: PLI Benefits)

Steel in India is no longer just metal. It is infrastructure, it is energy transition, it is Atmanirbhar Bharat in its most concrete form. The business case for entry has never been stronger — and waiting does not just reduce profits; it can cost businesses their position in one of the world’s great industrial transformations.